![]()

Use 8008 Exam Dumps (2021 PDF Dumps) To Have Reliable 8008 Test Engine

8008 PDF Recently Updated Questions Dumps to Improve Exam Score

NEW QUESTION 161

What is the 1-day VaR at the 99% confidence interval for a cash flow of $10m due in 6 months time? The risk free interest rate is 5% per annum and its annual volatility is 15%. Assume a 250 day year.

- A. 0

- B. 1

- C. 2

- D. 3

Answer: D

Explanation:

Explanation

The $10m cash flow due in 6 months is equivalent to a bond with a present value of 10m/(1.05)^0.5

=$9,759,000. Essentially, the question requires us to calculate the VaR of a bond.

The VaR of a fixed income instrument is given by Duration x Interest Rate x Volatility of the interest rate x z-factor corresponding to the confidence level.

In this case, since the question requires us to calculate the value "closest to" the correct answer, we can use an estimate for the modified duration of the bond as equal to 0.5 years/(1+r) = 0.5/1.05 = 0.47 years. The VaR would be given by 0.5 * 5% * 15% * 2.326 * sqrt(1/250) * 9,759,000 = $5,384 which is closest to $5,500.

Therefore Choice 'a' is the correct answer. Note that we have to multiply by sqrt(1/250) as the given volatility is annual and the question is asking for daily VaR. All other answers are incorrect.

NEW QUESTION 162

For a hypotherical UoM, the number of losses in two non-overlapping datasets is 24 and 32 respectively. The Pareto tail parameters for the two datasets calculated using the maximum likelihood estimation method are 2 and 3. What is an estimate of the tail parameter of the combined dataset?

- A. 2.23

- B. 0

- C. Cannot be determined

- D. 2.57

Answer: D

Explanation:

Explanation

For a number of processes, including many in finance, while a distribution such as the normal distribution is a good approximation of the distribution near the modal value of the variable, the same normal distribution may not be a good estimate of the tails. For this reason, the Pareto distribution is one of the distributions that is often used to model the tails of another distribution. Generally, if you have a set of observations, and you discard all observations below a threshold, you are left with what are called 'exceedances'. The threshold needs to be reasonably far out in the tail. If from each value of the exceedances you subtract the threshold value, the resulting dataset is estimated by the generalized Pareto distribution.

The Pareto distribution has a 'shape parameter'. The average of two Pareto distributions with tail parameters 1 and 2 ( is a Greek character, pronounced as 'sai' (saa-eee)), is the weighted average of 1 and 2 with weights proportional to the number of observations in the datasets underlying the distributions.

NEW QUESTION 163

Which of the following objectives are targeted by rating agencies when assigning ratings:

I. Ratings accuracy

II. Ratings stability

III. High accuracy ratio (AR)

IV. Ranked ratings

- A. I, II and III

- B. I and II

- C. II and III

- D. III and IV

Answer: B

Explanation:

Explanation

Rating agencies target both accuracy and stability when they assign ratings. These two objectives can sometimes conflict, so a balance needs to be struck between the two. Rating agencies do not target any particular 'accuracy ratio' or rankings. Therefore Choice 'c' is the correct answer.

NEW QUESTION 164

Which of the following is the best description of the spread premium puzzle:

- A. The spread premium puzzle refers to observed default rates being much less than implied default rates, leading to lower credit bonds being relatively cheap when compared to their actual default probabilities

- B. The spread premium puzzle refers to dollar denominated non-US sovereign bonds being priced a at significant discount to other similar USD denominated assets

- C. The spread premium puzzle refers to AAA corporate bonds being priced at almost the same prices as equivalent treasury bonds without offering the same liquidity or guarantee as treasury bonds

- D. The spread premium puzzle refers to the moral hazard implicit in the monoline insurance market

Answer: A

Explanation:

Explanation

Choice 'a' is the correct answer. The other choices represent non-sensical statements.

NEW QUESTION 165

If and are the expected rate of return and volatility of an asset whose prices are log-normally distributed, and a random drawing from a standard normal distribution, we can simulate the asset's returns using the expressions:

- A. - .

- B. - + .

- C. / .

- D. + .

Answer: D

Explanation:

Explanation

A standard model for representing asset returns in finance is the Geometric Brownian Motion process, and returns according to this model can be estimated by the expression given in Choice 'b'. Note that prices according to this model are log-normally distributed, and returns are normally distributed.

NEW QUESTION 166

CreditRisk+, the actuarial model for calculating portfolio credit risk, is based upon:

- A. the normal distribution

- B. the Poisson distribution

- C. the exponential distribution

- D. the log-normal distribution

Answer: B

Explanation:

Explanation

CreditRisk+ treats default as a binary event, ignoring downgrade risk, capital structures of individual firms in the portfolio or the causes of default. It uses a single parameter, or the mean default rate, and derives credit risk based upon the Poisson distribution. Therefore Choice 'c' is the correct answer.

NEW QUESTION 167

The results of 'desk-level' stress tests cannot be added together to arrive at institution wide estimates because:

- A. Desk-level stress tests focus on desk specific risks that may be minor or irrelevant in the larger scheme at the institution level.

- B. All of the above

- C. Desk-level stress tests tend to focus on extreme movements in risk parameters (such as volatility) without considering economy wide scenarios that may represent more realistic and consistent situations for the institution.

- D. Desk-level stress tests tend to ignore higher level risks that are relevant to the institution but completely outside the control of the individual desks.

Answer: C

Explanation:

Explanation

All the above listed reasons are valid explanations as to why an institution level stress test cannot be estimated by merely summing up the results of the stress tests of the individual desks.

NEW QUESTION 168

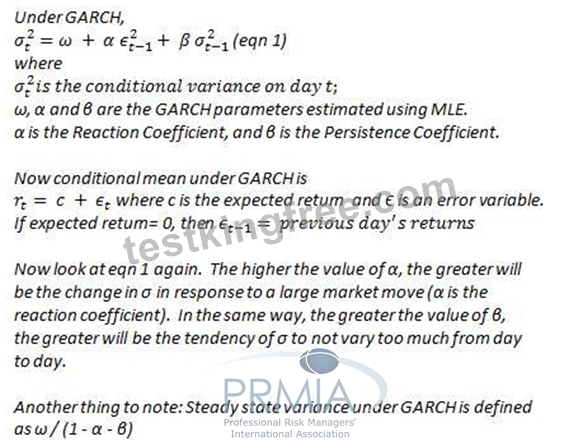

A risk analyst uses the GARCH model to forecast volatility, and the parameters he uses are = 0.001%, = 0.05 and = 0.93. Yesterday's daily volatility was calculated to be 1%. What is the long term annual volatility under the analyst's model?

- A. 3.54 %

- B. 0.25 %

- C. 7.94 %

- D. 0.22 %

Answer: A

Explanation:

Explanation

The correct answer is choice 'a'

Recall the following summary of the GARCH model. The long term variance in a GARCH model is given by

/(1 - - ). In this case, this works out to =SQRT(0.001/(1 - 0.05 - 0.93)) * SQRT(250) = 3.54%. Yesterday's volatility of 1% is irrelevant to the question.

NEW QUESTION 169

Credit exposure for derivatives is measured using

- A. Notional value of the derivative

- B. Current replacement value

- C. Forward looking exposure profile of the derivative

- D. Standard normal distribution

Answer: C

Explanation:

Explanation

Current replacement values are a very poor measure of the credit exposure from a derivative contract, because the future value of these instruments is unpredictable, ie is stochastic, and the range of values it can take increases the further ahead in the future we look. Therefore it is common for credit exposures for derivatives to be measured using forward looking exposure profiles, which are distributions of the expected value of the derivative at the time horizon for which credit risk is being measured. To be conservative, a high enough quintile of this distribution is taken as the 'loan equivalent value' of the derivative as the exposure. Choice 'c' is the correct answer.

The notional value of derivative contracts generally tends to be quite high and unrelated to their economic value or the counterparty exposure. Therefore notional value is irrelevant.

NEW QUESTION 170

As opposed to traditional accounting based measures, risk adjusted performance measures use which of the following approaches to measure performance:

- A. adjust both return and the capital employed to account for the risk undertaken

- B. adjust capital employed to reflect the risk undertaken

- C. adjust returns based on the level of risk undertaken to earn that return

- D. Any or all of the above

Answer: D

Explanation:

Explanation

Performance measurement at a very basic level involves comparing the return earned to the capital invested to earn that return. Risk adjusted performance measures (RAPMs) come in various varieties - and the key difference between RAPMs and traditional measures such as return on equity, return on assets etc is that RAPMs account for the risk undertaken. They may do so by either adjusting the return, or the capital, or both.

They are classified as RAROCs (risk adjusted return on capital), RORACs (return on risk adjusted capital) and RARORACs (risk adjusted return on risk adjusted capital).

NEW QUESTION 171

Which of the following is NOT true in respect of bilateral close out netting:

- A. Transactions are separated by transaction type and immediately settled separately at each's replacement value

- B. The net amount due is immediately receivable or payable

- C. All transactions are immediately closed out upon the occurrence of a credit event for either of the counterparties

- D. All transactions are netted against each other

Answer: A

Explanation:

Explanation

Choice 'b', Choice 'c' and Choice 'a' correctly describe a bilateral close out netting as recommended by the ISDA. However Choice 'd' is not correct as it suggests individual settlement of transactions without netting which is the whole point of bilateral close out netting.

NEW QUESTION 172

A Monte Carlo simulation based VaR can be effectively used in which of the following cases:

- A. All of the above

- B. Where analytical methods are too complex to effectively use

- C. D

- D. When returns are discontinuous or display large jumps

- E. When returns data cannot be analytically modeled

Answer: C

Explanation:

Explanation

Monte Carlo simulations can be effectively used in all cases where an analytical estimate of the VaR cannot be made for any reason - which may include complexity of portfolios, discontinuities or non-linearity in returns or just the plain unavailability of closed form analytical models. Therefore Choice 'd' is the correct answer.

NEW QUESTION 173

In respect of operational risk capital calculations, the Basel II accord recommends a confidence level and time horizon of:

- A. 99.9% confidence level over a 10 day time horizon

- B. 99.9% confidence level over a 1 year time horizon

- C. 99% confidence level over a 1 year time horizon

- D. 99% confidence level over a 10 year time horizon

Answer: B

Explanation:

Explanation

Choice 'd' represents the Basel II requirement, all other choices are incorrect.

NEW QUESTION 174

For a group of assets known to be positively correlated, what is the impact on economic capital calculations if we assume the assets to be independent (or uncorrelated)?

- A. Estimates of economic capital go down

- B. The impact on economic capital cannot be determined in the absence of volatility information

- C. Estimates of economic capital go up

- D. Economic capital estimates remain the same

Answer: A

Explanation:

Explanation

By assuming the assets to be independent, we are reducing the correlation from a positive number to zero.

Reducing asset correlations reduces the combined standard deviation of the assets, and therefore reduces economic capital. Therefore Choice 'b' is the correct answer.

Note that this question could also be phrased in terms of the impact on VaR estimates, and the answer would still be the same. Both VaR and economic capital are a multiple of standard deviation, and if standard deviation goes down, both VaR and economic capital estimates will reduce.

NEW QUESTION 175

If A and B be two debt securities, which of the following is true?

- A. The probability of simultaneous default of A and B is not dependent upon their default correlations, but on their marginal probabilities of default

- B. The probability of simultaneous default of A and B is greatest when their default correlation is negative

- C. The probability of simultaneous default of A and B is greatest when their default correlation is 0

- D. The probability of simultaneous default of A and B is greatest when their default correlation is +1

Answer: D

Explanation:

Explanation

If the marginal probability of default of two securities A and B is P(A) and P(B), then the probability of both of them defaulting together is affected by the default correlation between them. Marginal probability of default means the probability of default of each security on a standalone basis, ie, the probability of default of one security without considering the other security.

The relationship that expresses the probability of joint default of the two is given by the following expression:

It is easy to see that in a situation where the Default Correlation of A & B = 0, ie, the defaults are independent, the combined probability of default is P(A)*P(B), exactly what we would intuitively expect. Also in the other extreme case where the default correlation is equal to 1 and P(A) = P(B) = p, ie the securities behave in an identical way, the expression resolves to just p, which is what we would expect.

From the above relationship, it is clear that the probability of joint default of A and B is the greatest when default correlation between the two is equal to 1, ie the securities behave in an identical way. Therefore Choice

'a' is the correct answer.

NEW QUESTION 176

Changes in which of the following do not affect the expected default frequencies (EDF) under the KMV Moody's approach to credit risk?

- A. Changes in the risk free rate

- B. Changes in asset volatility

- C. Changes in the firm's market capitalization

- D. Changes in the debt level

Answer: A

Explanation:

Explanation

EDFs are derived from the distance to default. The distance to default is the number of standard deviations that expected asset values are away from the default point, which itself is defined as short term debt plus half of the long term debt. Therefore debt levels affect the EDF. Similarly, asset values are estimated using equity prices.

Therefore market capitalization affects EDF calculations. Asset volatilities are the standard deviation that form a place in the denominator in the distance to default calculations. Therefore asset volatility affects EDF too.

The risk free rate is not directly factored in any of these calculations (except of course, one could argue that the level of interest rates may impact equity values or the discounted values of future cash flows, but that is a second order effect). Therefore Choice 'b' is the correct answer.

NEW QUESTION 177

The returns for a stock have a monthly volatilty of 5%. Calculate the volatility of the stock over a two month period, assuming returns between months have an autocorrelation of 0.3.

- A. 8.062%

- B. 7.071%

- C. 5%

- D. 10%

Answer: A

Explanation:

Explanation

The square root of time rule cannot be applied here because the returns across the periods are not independent.

(Recall that the square root of time rule requires returns to be iid, independent and identically distributed.) Here there is a 'autocorrelation' in play, which means one period's returns affect the returns of the other period.

This problem can be solved by combining the variance of the returns from the two consecutive periods in the same way as one would combine the variance of different assets that have a given correlation. In such cases we know that:

Variance (A + B) = Variance(A) + Variance(B) + 2*Correlation*StdDev(A)*StdDev(B).

The standard deviation can be calculated by taking the square root of the variance.

Therefore the combined volatility over the two months will be equal to =SQRT((5%^2) + (5%^2) +

2*0.3*5%*5%) = 8.062%. All other answers are incorrect.

NEW QUESTION 178

Which of the following are valid techniques used when performing stress testing based on hypothetical test scenarios:

I. Modifying the covariance matrix by changing asset correlations

II. Specifying hypothetical shocks

III. Sensitivity analysis based on changes in selected risk factors

IV. Evaluating systemic liquidity risks

- A. I, II and III

- B. I, II, III and IV

- C. II, III and IV

- D. I and II

Answer: D

Explanation:

Explanation

Each of these represent valid techniques for performing stress testing and building stress scenarios. Therefore d is the correct answer. In practice, elements of each of these techniques is used depending upon the portfolio and the exact situation.

NEW QUESTION 179

Which of the following statements is true:

- A. Total expected losses are equal to the sum of individual underlying exposures while total unexpected losses are greater than the sum of unexpected losses on underlying exposures

- B. Both total expected losses and total unexpected losses are less than the sum of expected and unexpected losses on underlying exposures respectively

- C. Total expected losses are greater than the sum of individual underlying exposures while total unexpected losses are less than the sum of unexpected losses on underlying exposures

- D. Total expected losses are equal to the sum of expected losses in the individual underlying exposures while total unexpected losses are less than the sum of unexpected losses on underlying exposures

Answer: D

Explanation:

Explanation

Total expected losses which are average and anticipated are equal to the sum of expected losses in the underlying exposures. Total unexpected losses, which are the excess of worst case losses at a certain confidence level over the expected losses, benefit from the diversification effect and are lower than the sum of unexpected losses of the underlying exposures. Therefore Choice 'c' is the correct answer. The other choices are incorrect.

NEW QUESTION 180

A bank expects the error rate in transaction data entry for a particular business process to be 0.005%. What is the range of expected errors in a day within +/- 2 standard deviations if there are 2,000,000 such transactions each day?

- A. 80 to 120 errors in a day

- B. 0 to 200 errors in a day

- C. 60 to 80 errors in a day

- D. 90 to 110 errors in a day

Answer: A

Explanation:

Explanation

Error rates are generally modeled using the Poisson distribution. Recall that the Poisson distribution has only one parameter - - which is its mean and also its variance.

In the given case, the mean number of errors is 2,000,000 x 0.005% = 100. Since this is the variance as well, the standard deviation is 100 = 10. Therefore the range of outcomes within 2 standard deviations of the mean is 100 +/- (2*10) = 80 to 120 errors in a day.

NEW QUESTION 181

The standalone economic capital estimates for the three business units of a bank are $100, $200 and $150 respectively. What is the combined economic capital for the bank, assuming the risks of the three business units are perfectly correlated?

- A. 0

- B. 1

- C. 2

- D. 3

Answer: B

Explanation:

Explanation

Since the business units are perfectly correlated, we can get the combined EC as equal to the sum of the individual EC estimates. Therefore Choice 'a' is the correct answer.

NEW QUESTION 182

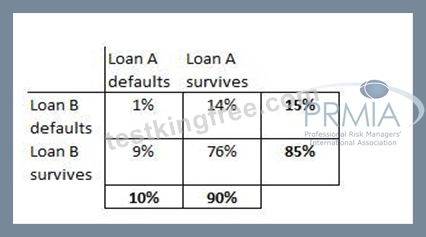

A portfolio has two loans, A and B, each worth $1m. The probability of default of loan A is 10% and that of loan B is 15%. The probability of both loans defaulting together is 1%. Calculate the expected loss on the portfolio.

- A. 0

- B. 1

- C. 2

- D. 3

Answer: A

Explanation:

Explanation

The easiest way to answer this question is to ignore the joint probability of default as that is irrelevant to expected losses. The joint probability of default impacts the volatility of the losses, but not the expected amount. One way to think about it is to think of asset portfolios, where diversification reduces risk (ie standard deviation) but the expected returns are nothing but the average of the expected returns in the portfolio. Just as the expected returns of the portfolio are not affected by the volatility or correlations (these affect standard deviation), in the same way the joint probability of default does not affect the expected losses. Therefore the expected losses for this portfolio are simply $1m x 10% + $1m x 15% = $250,000.

This can also be seen from the lens of a joint probability distribution as follows:

There are four possibilities for this portfolio:

- Only loan A defaults: loss of $1m: 9% probability

- Only loan B defaults: loss of $1m: 14% probability

- Both loan A and B default: loss of $2m: 1% probability

- Neither A nor B default: loss of $0m: 76% probability

Therefore the expected losses on the portfolio are ($1m x 9%) + ($1m x 14%) + ($2m x 1%) + ($0m x 76%) =

$250,000.

(Notes: How is the above table calculated? The totals (10%, 90%, 15% and 85%) are filled in first. The top left cell (both A & B default) is given as 1%. We can now calculate the rest of the cells as the totals are known.)

NEW QUESTION 183

Which of the following best describes Altman's Z-score

- A. A calculation of default probabilities

- B. A numerical computation based upon accounting ratios

- C. A standardized z based upon the normal distribution

- D. A regression of probability of survival against a given set of factors

Answer: B

Explanation:

Explanation

Choice 'c' correctly describes Altman's z-score. All other choices are incorrect.

NEW QUESTION 184

Which of the following statements are true?

I. Retail Risk Based Pricing involves using borrower specific data to arrive at both credit adjudication and pricing decisions II. An integrated 'Risk Information Management Environment' includes two elements - people and processes III. A Logical Data Model (LDM) lays down the relationships between data elements that an organization stores IV. Reference Data and Metadata refer to the same thing

- A. All of the above

- B. I, II and III

- C. I and III

- D. II and IV

Answer: C

Explanation:

Explanation

Statement I is correct. Retail Risk Based Pricing (RRBP) involves the use of borrower specific data (such as FICO scores, average balances etc) to arrive at credit decisions. These 'retail' credit decisions may include decisions on whether to grant a line of credit, a mortgage, issue a credit card, or any of the various other retail activities a bank may be dealing with. At the same time, this data can also be used to price the product, in addition to providing a yes or no credit decision so that risky borrowers are charged more than less risky borrowers.

Statement II is not correct, because an integrated Risk Information Management Environment includes three elements - people, processes and technology (and not just people and processes).

Statement III is correct. An LDM is a blue print of an organization's data, and describes the relationships between the various data elements.

Statement IV is not correct because reference data and metadata are not the same thing. Reference data refers to relatively static data, such as customer name (while actual transactions may not be so static). Metadata refers to data about data, and is stored in a data dictionary.

Therefore Choice 'b' is the correct answer and the rest are incorrect.

NEW QUESTION 185

......

8008 Dumps Full Questions with Free PDF Questions to Pass: https://www.testkingfree.com/PRMIA/8008-practice-exam-dumps.html